High Potential BESS Ecosystem: A Reasonably valued Small Cap pivoting with Massive Order book.

How an undervalued infrastructure player is leveraging domestic integration to capture India’s structural energy storage supercycle.

The deployment of Battery Energy Storage Systems (BESS) is no longer a discretionary infrastructure upgrade; it is a structural mandate. As grids globally transition from dispatchable fossil fuels to intermittent renewable sources, energy storage is the critical bottleneck.

Here is a structured analysis of the strategic imperative for BESS, alternative technologies, the competitive landscape, and inherent risks.

The Strategic Imperative: Why BESS?

The rapid adoption of BESS is driven by its unique operational characteristics compared to legacy grid infrastructure:

Intermittency Resolution: Solar and wind generation are weather-dependent. BESS captures excess generation during peak production hours (e.g., midday solar) and discharges it during peak demand hours (evening), effectively flattening the “duck curve.”

Grid Stability & Ancillary Services: BESS provides instantaneous sub-second response times for frequency regulation and voltage control, services that traditional thermal plants cannot match.

Geographic Flexibility & Deployment Speed: Unlike pumped hydro, BESS is modular. A 100 MWh containerized BESS facility can be deployed in months near demand centers or existing solar parks, bypassing complex geographic requirements and years of environmental clearances.

Declining LCOS (Levelized Cost of Storage): The persistent drop in lithium-ion cell prices is making battery storage increasingly competitive against natural gas peaker plants.

Technological Alternatives to Lithium-Ion BESS

While lithium-ion currently dominates short-to-medium duration storage (2 to 4 hours), the broader energy storage matrix includes several alternatives, each with specific use cases:

Pumped Hydro Storage (PHS): The legacy giant of grid storage. It involves pumping water to a higher elevation reservoir during low-demand periods and releasing it through turbines during peak demand.

Advantage: Massive scale, long lifespan (50+ years), low cost per kWh for long-duration storage.

Disadvantage: Extremely capital-intensive, 5-to-10-year construction timelines, and severe geographic dependencies.

Green Hydrogen: Utilizing excess renewable power for electrolysis to create hydrogen, which can later be burned or run through fuel cells.

Advantage: Excellent for long-duration (seasonal) storage and deep decarbonization of heavy industries.

Disadvantage: Low round-trip efficiency (often below 40%) and currently lacks widespread transport and storage infrastructure.

Alternative Battery Chemistries: Sodium-ion (Na-ion) and Flow Batteries (e.g., Vanadium Redox).

Advantage: Sodium-ion reduces reliance on lithium and cobalt; Flow batteries offer scalable, long-duration storage without degradation.

Disadvantage: Currently trailing lithium-ion in energy density and manufacturing scale.

Mechanical / Thermal Storage: Technologies like flywheels (for immediate, short-burst frequency regulation) and molten salt (often paired with Concentrated Solar Power).

The Competitive Landscape: Major Players

The BESS value chain is highly fragmented, segmented into cell manufacturers, system integrators, and developers.

Global Tier-1 Cell Manufacturers: The supply chain is dominated by Chinese and Korean entities controlling the raw chemistry and cell production.

Key Players: CATL (China), BYD (China), LG Energy Solution (South Korea), Samsung SDI (South Korea).

Global System Integrators: Companies that procure cells and build the software/hardware architecture (EMS/PMS) for grid deployment.

Key Players: Fluence (Siemens/AES joint venture), Tesla Energy (Megapack), Wärtsilä.

The Indian Ecosystem: Driven by aggressive government targets and PLI (Production Linked Incentive) schemes, the domestic market is maturing rapidly.

Conglomerates & Utilities: Tata Power (aggressive EPC and developer), Reliance Industries & Sterling & Willson (building gigafactories for end-to-end integration), JSW Energy.

Advait Energy transition and Bondada Engineering (Pivot and mixed revenue)

Legacy Battery Majors: Amara Raja and Exide Industries (pivoting from lead-acid to lithium-ion cell manufacturing).

Key Risk Matrix

Investing in or deploying BESS infrastructure carries distinct systemic and operational risks:

Supply Chain Vulnerability: The absolute reliance on lithium, cobalt, nickel, and graphite—minerals predominantly mined or refined in China and parts of Africa/South America—exposes the sector to geopolitical friction, export controls, and severe price volatility.

Technological Obsolescence: The rapid pace of R&D means today’s state-of-the-art Lithium Iron Phosphate (LFP) containers could be outpaced economically by Sodium-ion or Solid-State batteries within a standard 12-year project lifecycle, potentially impacting asset terminal values.

Execution and Fire Safety: Lithium-ion systems carry the risk of thermal runaway. Poor integration of Battery Management Systems (BMS) or substandard HVAC controls can lead to catastrophic fires, resulting in total asset loss and massive liability.

Regulatory & Tariff Risks: The sector relies heavily on evolving grid regulations and long-term Power Purchase Agreements (PPAs). Aggressive bidding by developers to win market share can lead to compressed IRRs, leaving minimal margin for error if cell replacement costs rise unexpectedly.

PACE DIGITEK

Pace Digitek Limited operates as an end-to-end solutions provider primarily within the telecom passive infrastructure and energy sectors. It holds a growing footprint in the Battery Energy Storage Systems (BESS) and renewable-linked project domains. Following its transition from a private to a public entity and an IPO in October 2025, the company has positioned itself as an integrated EPC (Engineering, Procurement, and Construction), operations and maintenance (O&M), and Built-Own-Operate (BOO) player.

Market Cap: ~₹4,000 Cr

Current Price: ~₹185.18

52-Week Range: ₹139.50 - ₹232.20

P/E Ratio (TTM): ~13.79 (Sector P/E: ~16.8 - 22.4)

P/B Ratio: ~1.74 - 1.99

ROE (TTM): 32.65% - 34.04%

ROCE (TTM): 40.73% - 42.84%

Debt-to-Equity: ~0.38 - 0.45 (indicates a relatively unleveraged balance sheet).

Investment Thesis

Pace Digitek presents a compelling GARP (Growth at a Reasonable Price) opportunity, trading at a discount to its peers (P/E of 13.8x vs. sector average >16x) while demonstrating a rapid pivot toward high-margin, high-growth energy projects. The core thesis rests on its massive order book execution visibility. With ~₹6,460 Cr in recent order inflows heavily skewed toward energy (₹5,815 Cr) rather than its legacy telecom business, Pace is transforming into a BESS and renewable energy proxy. The balanced mix of EPC, BOO, and supply contracts provides both near-term cash generation and long-term annuity visibility, derisking the revenue stream.

Potential

The reported ₹6,460 Cr in order inflows provides multi-year revenue visibility, significantly dwarfing its trailing revenues. Management guidance suggests ~40% of the energy order book will be executed in FY27, which should drive substantial topline acceleration.

The recent ₹702 Cr order from Damodar Valley Corporation (DVC) for a 25 MW/500 MWh BESS project validates its capabilities in the rapidly expanding energy storage market, a critical bottleneck for India’s renewable grid integration.

An exclusive OEM deal with NEC XON Systems opens the Southern African market (South Africa, Botswana, Mozambique, Namibia, Mauritius) for BESS and energy solutions, providing an international growth vector.

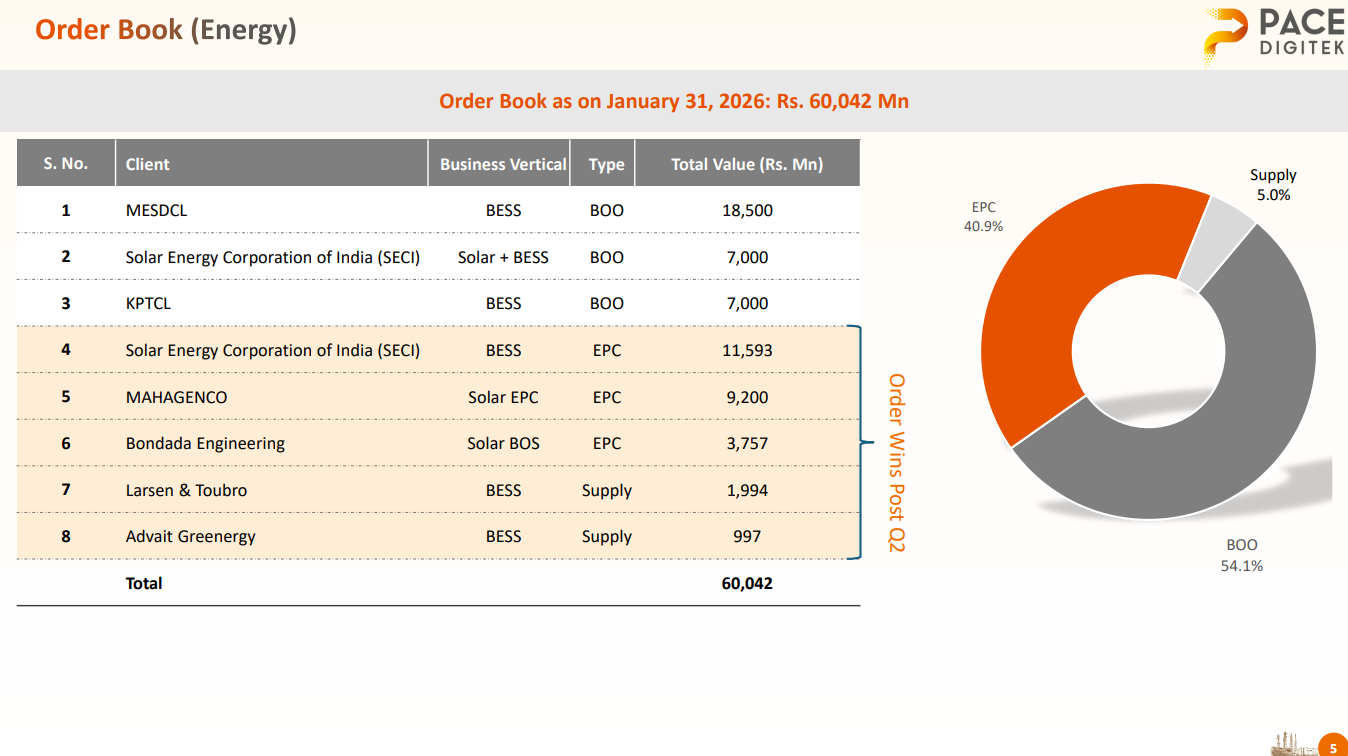

As of January 31, 2026, Pace Digitek’s total unexecuted order book stands at a robust Rs. 84,678 Mn. The composition reveals a deliberate strategic pivot toward the energy vertical, which now dominates future revenue visibility.

Energy Segment: Rs.60,042 Mn (71% of Total)

The energy portfolio is heavily tilted toward long-term asset creation, structurally shifting the company toward an annuity-based cash flow model over the next decade.

BOO (Built-Own-Operate): 54.1%

Comprises major orders like the Rs. 18,500 Mn MSEDCL project and Rs. 7,000 Mn SECI Solar+BESS project. These require upfront CapEx (funded at a ~75:25 debt-to-equity ratio) but yield an equity IRR of ~14% over 12-to-25-year power purchase agreements.

EPC: 40.9%

Includes the Rs. 11,593 Mn SECI BESS project and Rs. 9,200 Mn MAHAGENCO Solar EPC project. Provides near-term revenue recognition and cash flow to fund the equity portion of the BOO pipeline. Project-level margins track at 8-10%.

Supply: 5.0%

Direct equipment sales to clients like L&T and Advait Greenergy, capturing a 13-15% product margin.

Telecom & ICT Segment: Rs. 24,637 Mn (29% of Total)

This segment is primarily EPC-driven, characterized by higher near-term margins but greater working capital intensity (120–150 days) due to government tender retention money.

Tower Infra EPC: 78.7% (Anchored by a Rs. 16,100 Mn BSNL contract).

+1

Telecom Power Equipment: 7.7%.

Tower Infra & OFC: 7.5%.

Tower Infra EPC + Services: 6.1%.

Revenue Bifurcation & Margin Dynamics (Q3 FY2026)

For Q3 FY2026, the company reported Consolidated Revenue of Rs. 6,440 Mn (up 13.5% YoY) and an EBITDA margin of 18.3%. The execution mix during this quarter presents several critical accounting and margin nuances:

+2

Margin Mix Shift: Current profitability is blended. The legacy telecom business is temporarily inflating the overall margin profile, yielding an 18% product margin plus a 13-15% project margin on specific tower erection cycles. As the heavier volume of BESS EPC executes (which carries an 8-10% project margin on top of a 13-15% product margin), consolidated EBITDA margins are expected to structurally stabilize in the 13-15% range.

+4

Accounting Eliminations (The BOO Effect): Standalone revenue for Q3 was Rs. 5,420 Mn. The discrepancy between standalone and consolidated figures is primarily due to intercompany eliminations. When the parent company (Pace Digitek) or its manufacturing arm (Lineage Power) supplies products or EPC services to its wholly-owned Special Purpose Vehicles (SPVs) under the new TransGreenX platform for BOO projects, those “sales” cannot be recognized as revenue on the consolidated P&L. Instead, they are capitalized on the balance sheet. For context, the company recorded Rs. 1,674 Mn in asset creation under the energy vertical as of December 2025.

Risks

Execution Risk & Working Capital Intensity: The sheer scale of the new order book compared to historical revenues presents significant execution challenges. EPC and BOO contracts require stringent working capital management; any deterioration in debtor days or inventory turnover could strain cash flows.

Input Cost Volatility: Exposure to raw material price fluctuations (metals, lithium-ion components for BESS) could compress gross margins if costs cannot be entirely passed on to clients.

Client Concentration: While diversifying, reliance on a few large government or quasi-government tenders (like DVC) exposes the company to order lumpiness and potential payment delays typical of public sector undertakings.

Competition in EMS/BESS: The Electronic Manufacturing Services (EMS) and BESS spaces are increasingly crowded, requiring continuous technological adaptation and cost competitiveness.

To conduct similar in depth analysis, explore nivezo.in Deep Research.

AI -Powered Investment Intelligence Platform

Sector & Macro View

The macro environment for Pace Digitek is highly favorable, driven by twin tailwinds in India’s grid modernization and telecommunications expansion. The company is positioned at the intersection of these two capital-intensive transitions.

BESS and Energy Storage: The integration of intermittent renewable energy into the national grid requires massive storage capacity. Government estimates project a requirement of 236 GWh of Battery Energy Storage Systems (BESS) by 2030 to support 500 GWh of renewable energy. Demand is expected to accelerate sharply between 2027 and 2032. Policy frameworks, such as the National Electricity Policy 2026 and local content mandates (often requiring a minimum of 20% domestic content), create a structural moat for local manufacturers.

+4

Arbitrage on Import Duties: A critical micro-driver within the macro environment is the tariff structure. Importing raw lithium-ion cells attracts a 5% duty, whereas importing finished BESS containers from China incurs a duty of approximately 10%. This raw material vs. finished goods spread yields a direct margin advantage for domestic pack-to-container assemblers like Pace Digitek, effectively competing with Chinese imports on an absolute cost basis while offering superior localized operational and maintenance support.

+4

Telecom Infrastructure: While energy is the primary growth vector, the legacy telecom sector provides a stable foundation. Driven by data consumption, 5G network densification, and broader fiberisation, the total number of telecom towers in India is projected to scale from 805,000 in FY24 to between 1.01 million and 1.03 million by FY28.

Moat

Pace Digitek competes with players like Indus Towers (telecom infra), HFCL (telecom equipment), and emerging energy storage companies.

Moat: Pace’s primary advantage is its integrated capability. It doesn’t just manufacture; it designs, executes (EPC), and operates (O&M/BOO) telecom and energy assets. This end-to-end service model increases client stickiness. Its legacy in telecom passive infrastructure provides a stable base from which it is aggressively expanding its higher-margin energy portfolio.

Commentary on Cashflow

Management anticipates an overall improvement in working capital intensity going forward, supported by tighter receivables management and a favorable shift in the revenue mix toward the energy segment.

It is also critical to delineate the EPC business from the BOO (Built-Own-Operate) developer model. While EPC contracts demand short-term working capital lockups, the BOO model fundamentally alters the cash flow profile. BOO projects do not strain short-term working capital in the same manner; instead, they require long-term capital allocation where term loans are repaid over a 10-year horizon within a 12-year project lifecycle.

Recent Happenings

May 2026: Secured a massive ₹702 Cr EPC+O&M order from Damodar Valley Corporation for a 25 MW/500 MWh BESS project in Jharkhand.

April 2026: Signed an exclusive OEM deal with NEC XON Systems for marketing and distributing BESS and energy solutions across Southern Africa.

April 2026: Announced total FY26 order inflows of ₹6,459.70 Cr, with the energy segment contributing ₹5,814.70 Cr.

April 2026: Issued a postal ballot notice seeking shareholder approval for substantial Related Party Transactions (~₹9,397 Cr) involving material subsidiaries, primarily for the sale/purchase of products and services, indicating intra-group restructuring or large-scale internal supply chain alignment for order execution.

February 2026: Q3 FY26 results showed EPS of ₹3.85 (up from ₹3.62 YoY) and Net Income of ₹75.84 Cr, with profit margins expanding to 12%.

March 2026: Received an LoA for ₹22.64 Cr from North Western Railway for lattice towers.

Investment Summary

Valuation Disconnect: Trading at a P/E of ~13.8x, Pace Digitek is undervalued relative to the market and its sector, especially given its high ROE (~34%) and ROCE (~42%).

Transformational Order Book: The ₹6,460 Cr FY26 order inflow, overwhelmingly in energy (BESS/Renewables), provides explosive multi-year revenue visibility, far exceeding historical run rates.

Strategic Pivot: The company is successfully transitioning from a legacy telecom infra provider to an integrated energy storage (BESS) and renewable EPC play, capturing significant macro tailwinds.

Balanced Revenue Model: A mix of EPC (near-term revenue), BOO (long-term annuity), and O&M contracts structurally derisks the cash flow profile.

Execution is the Catalyst: The primary risk is the management’s ability to execute a suddenly massive order book while managing working capital efficiently; successful execution of the DVC BESS project will be a critical proof point.

Confidence Level: High (Given the valuation margin of safety and contracted order book visibility).

Expected Timeframe: 12-18 months (Allowing time for execution of the newly acquired order book to reflect in quarterly earnings).