Laurus Labs: High-Precision Chemistry Factory entering in OLED Innovation.

A diversified "Science-at-Scale" company. They are using their chemical expertise to enter high-barrier industries: CDMO (Pharma), Gene Therapy (Biotech), and Advanced Materials (Tech/OLED).

Think of Laurus Labs not just as a “Pharma” company, but as a High-Precision Chemistry Factory. Traditionally, they were known as the “King of ARVs” (Anti-Retrovirals), supplying the active ingredients for HIV medicines globally. Today, they have pivoted to become a science-led manufacturer that makes everything from generic drugs to cancer cures and now, high-tech display materials.

We will discuss this in detail but before that let’s dive into what Laurus and LORDIN are doing currently.

Laurus Labs

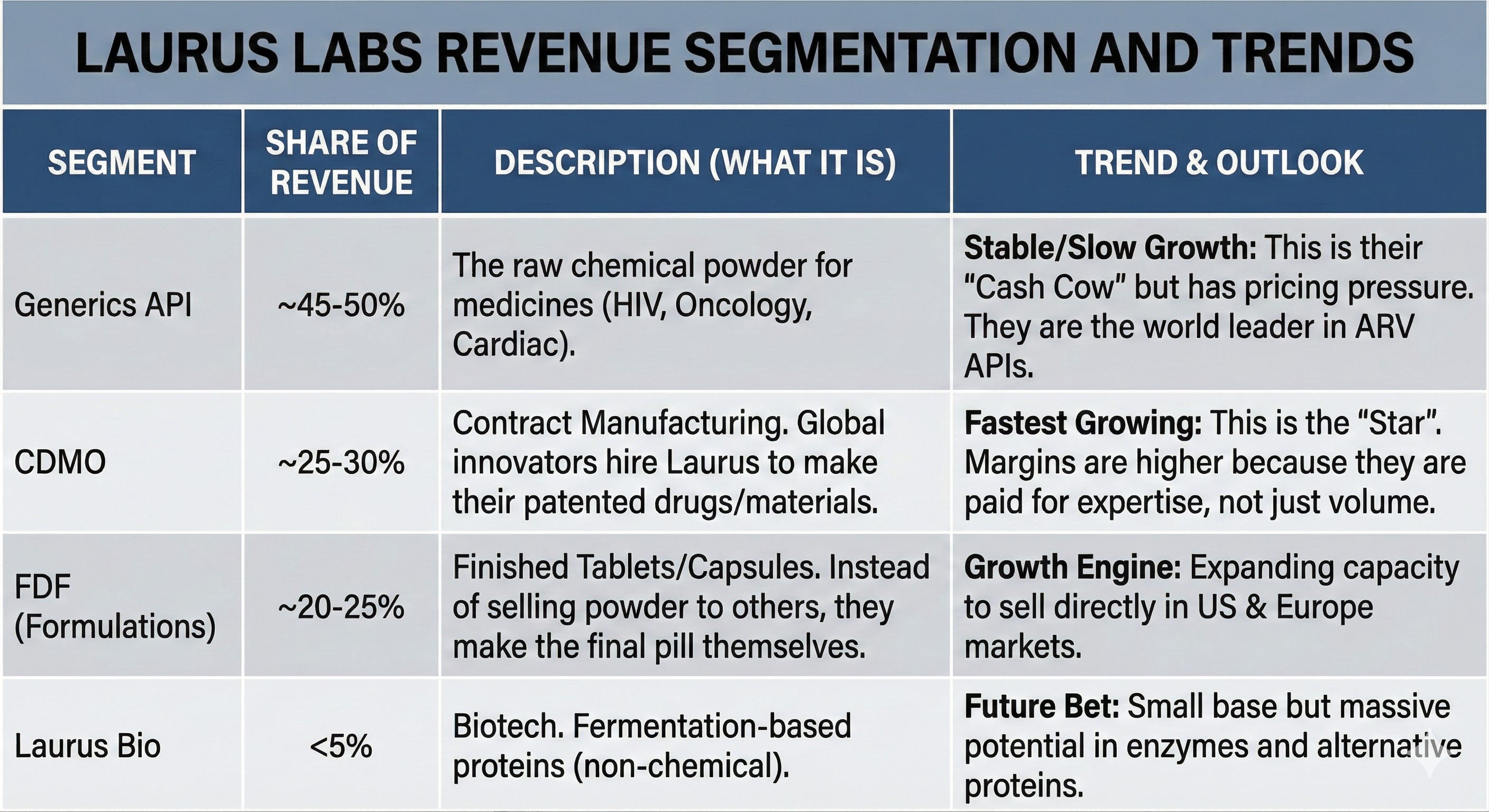

Laurus has aggressively shifted its revenue mix to reduce dependence on commoditized drugs. Here is the approximate split based on recent FY25 trends:

Innovation: From “Copying” to “Creating”

Laurus is moving up the value chain. Instead of just reverse-engineering old drugs (Generics), they are now solving complex problems.

A. The “ImmunoACT” Revolution (Cancer Cure)

The Deal: Laurus owns a significant stake (~34%) in ImmunoACT, an IIT Bombay spin-off.

The Product: NexCAR19. This is India’s first indigenous CAR-T Cell Therapy.

Why it’s huge: CAR-T therapy involves taking a patient’s blood, genetically engineering their T-cells to kill cancer, and putting them back. In the US, this costs ~$400,000. Laurus/ImmunoACT is doing it for ~1/10th the cost. This is a massive humanitarian and commercial innovation for treating blood cancers (Leukemia/Lymphoma).

B. Precision Fermentation (Laurus Bio)

They don’t just use chemical reactors; they use giant bio-fermenters (like brewing beer, but for proteins).

Innovation: They manufacture Growth Factors (proteins) used in:

Stem Cell Research.

Cultured Meat (Lab-grown meat industry requires these proteins to grow cells).

Cosmeceuticals (high-end skin care ingredients).

New Areas: The “Non-Pharma” Bets

This is where the LORDIN partnership we mentioned earlier fits in. Laurus is applying its chemistry skills to completely new industries.

I. Animal Health

Laurus is aggressively entering the veterinary space, specifically manufacturing drugs for pets and livestock.

They have set up dedicated blocks for Animal Health APIs because regulations often require separating human and animal drug lines.

II. Crop Science

They have signed multi-year manufacturing deals with global agrochemical giants.

Focus: They aren’t making cheap pesticides; they are making advanced intermediates for new-age crop protection molecules that are safer and more targeted.

LORDIN Co., Ltd. (South Korea)

Established: February 2020 (Young Startup, ~5 years old)

Scale: Small Deep-Tech Team (~30 Employees)

Headquarters: Hwaseong, South Korea (Near Samsung/LG semiconductor hubs)

Status: Pre-IPO / Series B Stage (Not a public giant yet)

Financials & Backing

Total Funding Raised: ~$11.6 Million (approx. ₹95-100 Crores)

Revenue: Generating early revenue (mostly grants and sample sales), but not yet profitable or at commercial mass-production scale.

Key Investors (The “Smart Money”):

Korea Development Bank (KDB): State-owned bank backing strategic tech.

POSCO Venture Capital: The VC arm of POSCO (steel/materials giant).

IBK (Industrial Bank of Korea): Another major government-backed lender.

Smilegate Investment: A prominent Korean VC.

The Brain Behind It

Founder & CEO: Dr. Oh Hyoung-yun

Credibility: He is a veteran of the industry.

Former Researcher at LG Electronics (11 years).

Former Team Leader at LG Display.

He didn’t just study this; he built OLED products for LG and Samsung before starting his own company to fix the “Blue” problem.

Now, let’s dig into the new frontier Laurus is getting into as there is a great amount of buzz on social media pointing on why Laurus has overdiversified by getting into OLED Display thing.

Let’s understand this one by one.

The Partnership: Laurus Labs (India) x LORDIN (South Korea)

The Deal: Laurus Labs is partnering with LORDIN, a South Korean innovator, to manufacture and supply advanced OLED materials.

The collaboration focuses specifically on Blue Phosphorescent OLED emitters—often considered the “Holy Grail” of the display industry due to the historical difficulty in stabilizing blue light emission compared to red and green.

The Role of Laurus: Laurus Labs is leveraging its massive capacity for chemical synthesis (used for making drugs) to manufacture the complex organic molecules needed for OLED screens.

The Role of LORDIN: They provide the proprietary technology and patents. LORDIN is not a mass manufacturer; they are an R&D powerhouse. They need a partner who can scale up production of high-purity chemicals—exactly what Laurus does best.

The Innovation: Cracking the “Blue” Problem

The specific technology involved here is arguably the “Holy Grail” of the display industry.

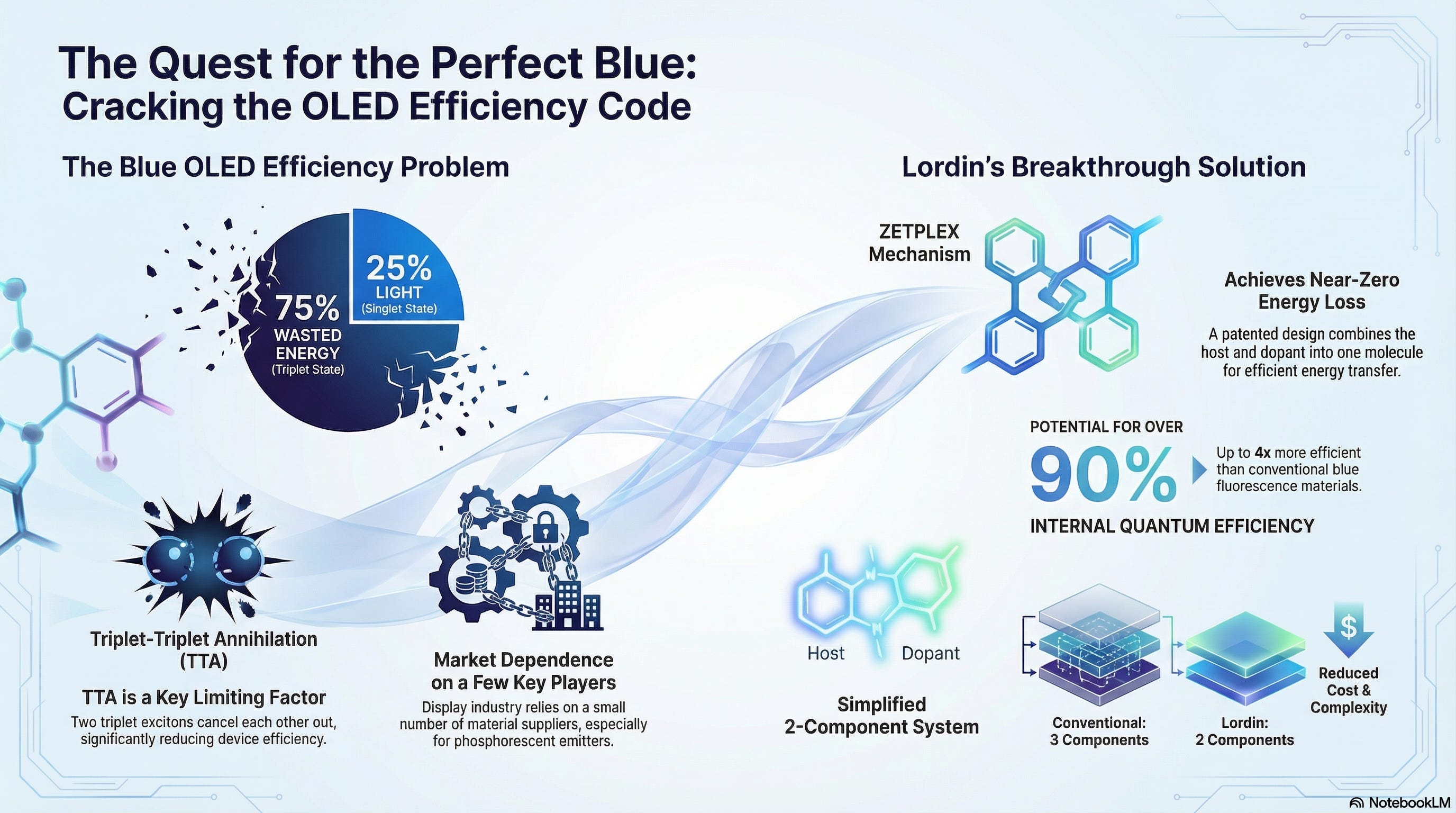

The Problem: OLED screens have historically struggled with Blue light. Red and Green organic materials are efficient and long-lasting, but Blue materials die quickly and consume too much power.

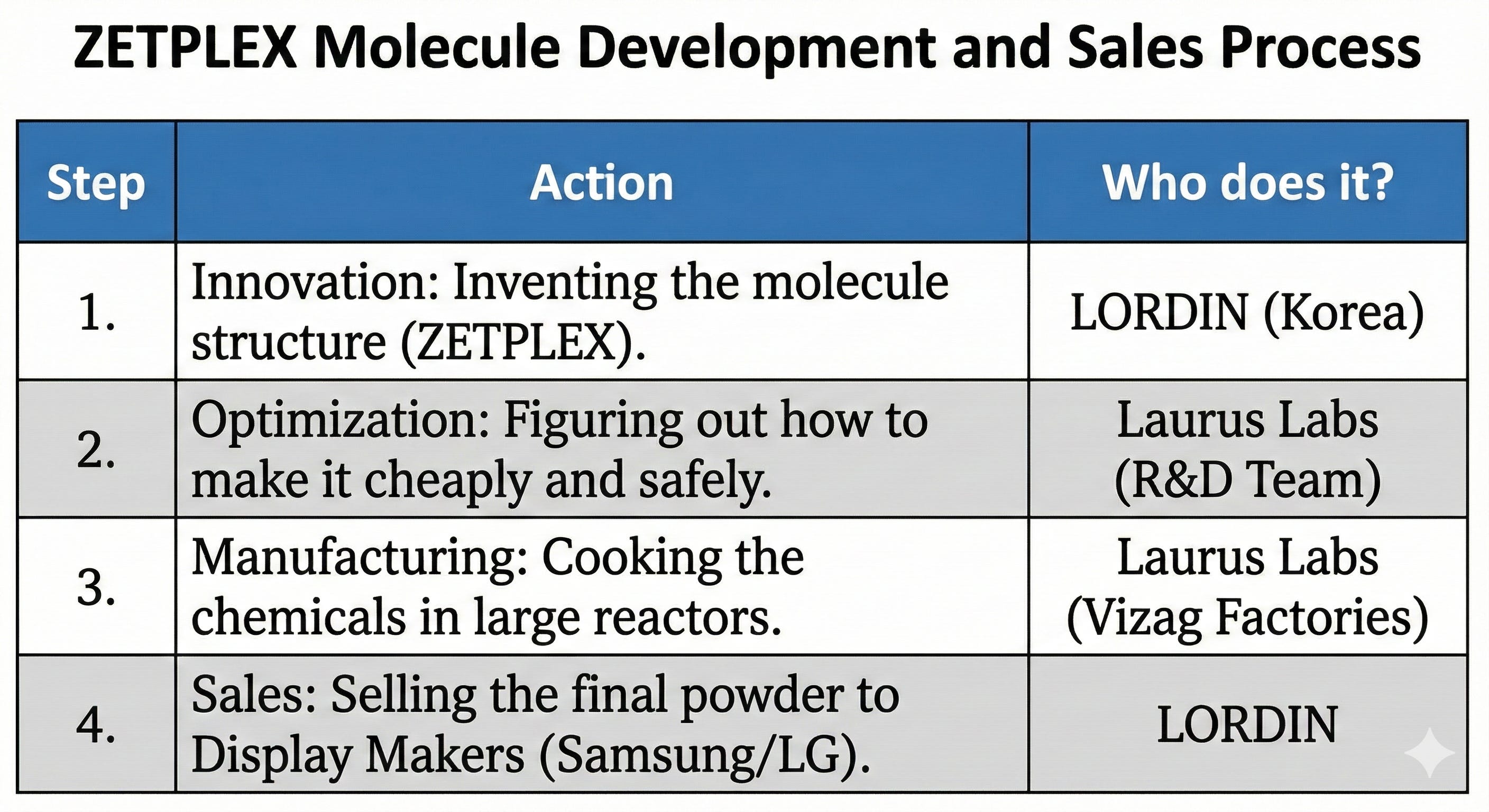

LORDIN’s Breakthrough (ZETPLEX): LORDIN holds patents for a technology called Zero-radius Intra-molecular Energy Transfer (ZETPLEX).

This technology creates a High-Efficiency Blue OLED Emitter.

It aims to make blue pixels 4x more efficient than current standards.

Efficiency: Claims >90% internal light emission efficiency (triple the ~25% of current fluorescent blue emitters).

Longevity: Recent data (Dec 2025) suggests their material lifetime is finally suitable for commercial AMOLED displays (smartphones, TVs).

Why this matters: If Laurus Labs manufactures the material that finally solves the “Blue OLED” efficiency problem, they become a critical link in the supply chain for next-generation iPhones, Samsung phones, and EV displays.

Market Context (2025-2026 Outlook)

Market Size: The global OLED materials market is valued at approximately $29.7 billion (2024) and is projected to grow at a CAGR of ~18% through 2033.

Primary Drivers:

•IT OLED Shift: Apple and other OEMs are aggressively transitioning tablets and laptops to OLED screens, significantly increasing the surface area (and thus material volume) required per device compared to smartphones.

•Automotive: Digital cockpits in EVs are driving demand for high-durability OLED materials.

The “Context”: Why a Pharma Company?

It might seem strange for a drug maker to make TV screen materials, but chemically, they are very similar.

1. The “Scale-Up” Problem (The Core Help)

LORDIN is an R&D company. They synthesize their “Blue OLED” material in small glass beakers (grams). To sell to Samsung or LG, they need to supply metric tons of this material every month.

What Laurus Does: Laurus takes LORDIN’s gram-level recipe and figures out how to make it in 5,000-liter reactors without causing explosions or ruining the quality.

Why Laurus? Scaling up complex organic chemistry is incredibly difficult. Laurus has been doing this for HIV and Cancer drugs for 15 years. They are applying their CDMO (Contract Development & Manufacturing) playbook to display materials.

2. The “Purity” Barrier (The Technical Edge)

This is the most critical technical reason for the partnership.

The Requirement: OLED materials must be “Sublimation Grade” pure. This means 99.999% purity. A single microscopic dust particle or metal ion in the material can cause a “dead pixel” on a smartphone screen.

The Overlap: Pharmaceutical companies are the only other industry obsessed with this level of purity (Parts Per Billion). Laurus Labs already has the clean rooms, filtration systems, and analytical tools (Chromatography) to guarantee this purity. A standard chemical factory would fail here.

3. IP Protection (The Trust Factor)

The Fear: If LORDIN gave their recipe to a generic chemical manufacturer in China, there is a high risk the recipe could be stolen or copied.

The Laurus Shield: Laurus Labs is a trusted partner for global giants like Pfizer and Merck. They have strict IP protocols because they handle patented drug secrets daily. For a Korean company like LORDIN, Laurus offers a “safe zone” to manufacture proprietary tech without risking IP theft.

4. Supply Chain De-risking (The “China+1” Strategy)

The Korean Context: Currently, South Korean display makers (Samsung/LG) import a lot of their raw materials from China. They are desperate to diversify.

The Solution: By partnering with Laurus, LORDIN creates a supply chain that bypasses China. They can tell Samsung: “We have a high-quality supply source in India that is distinct from the Chinese ecosystem.”

What can go wrong?

Let’s understand this one by one starting from what problem LORDIN is solving.

1. The Core Problem: The “Blue” Weakness

An OLED screen is made of three color pixels: Red, Green, and Blue.

Red & Green: These pixels use a technology called Phosphorescence (patented by a US company called UDC). They are 100% efficient—almost all electricity turns into light.

Blue: Blue pixels currently use an older technology called Fluorescence. They are only 25% efficient. The rest of the electricity turns into heat, which kills the battery and burns out the screen.

The Holy Grail: The entire industry is racing to find a “High-Efficiency Blue” that is stable. Whoever finds it first will likely be in every iPhone, Galaxy, and EV car dashboard for the next decade.

2. Where LORDIN Fits (The Technology)

LORDIN (the Laurus partner) is betting on a specific solution called “Hyperfluorescence” / ZETPLEX.

The Claim: They claim their patented technology can make Blue pixels 4x more efficient (matching Red/Green) without sacrificing lifespan.

The Competitive Edge: Their approach aims to be cheaper and purer (narrower color spectrum) than the rival solutions being developed by the giants.

3. The Competitive Landscape (Who are they fighting?)

LORDIN is a small innovator entering a battlefield dominated by massive global chemical giants. Here is the hierarchy:

A. The Monopoly (The Final Boss)

Universal Display Corp (UDC) - USA:

Status: They essentially own the “OLED market.” Every phone maker pays them royalties for Red and Green.

The Threat: UDC has been working on their own “Blue Phosphorescence” (PHOLED) for 10 years. If they succeed and launch it commercially (expected late 2025/2026), they could lock up the market before LORDIN even starts.

B. The Direct Tech Rivals (The Other Startups)

Kyulux (Japan):

They are also working on “Hyperfluorescence” (similar to LORDIN). They are heavily funded and backed by Samsung and LG. This is LORDIN’s most direct “peer” competitor.

Idemitsu Kosan (Japan):

The current “King of Blue.” They supply the inefficient blue materials used in iPhones today. They are aggressively researching their own next-gen blue to defend their territory.

C. The Buyers (The Gatekeepers)

Samsung Display & LG Display:

LORDIN + Laurus don’t sell to you; they sell to Samsung/LG. These two companies test materials rigorously. If LORDIN’s “Blue” fails a stress test (e.g., burns out after 5,000 hours), they are out.

Summary of the Bet

If it works: Laurus/LORDIN solves the “Blue Problem.” Their material gets designed into next-gen screens. Revenue potential is massive because every OLED screen needs Blue.

LORDIN’s announcement in December 2025 that it has "verified commercial feasibility" is the signal that they are ready to move from R&D labs to actual production lines—likely starting in China or with niche high-end applications

The biggest Risk: UDC launches their Blue PHOLED first, or Samsung decides to stick with Idemitsu.

Innovation Context for India: This is historically significant. Usually, India imports these high-tech chemicals. If Laurus succeeds, India will be exporting the core “active ingredient” of future displays, much like it exports the active ingredients of medicines today.

To conduct similar in depth analysis, explore nivezo.in Deep Research.

beautifuly articulated... and a very insightful deep dive

This actually shows laurus labs don't have laser point focus. So in future ROCE expansion is not possible and wealth is creation for investors will be a question mark